Finance Act 1982

1982 c. 39An Act to grant certain duties, to alter other duties, and to amend the law relating to the National Debt and the Public Revenue, and to make further provision in connection with Finance.

X1I1X2Most Gracious Sovereign,

WE, Your Majesty’s most dutiful and loyal subjects, the Commons of the United Kingdom in Parliament assembled, towards raising the necessary supplies to defray Your Majesty’s public expenses, and making an addition to the public revenue, have freely and voluntarily resolved to give and grant unto Your Majesty the several duties hereinafter mentioned; and do therefore most humbly beseech Your Majesty that it may be enacted, and be it enacted by the Queen’s most Excellent Majesty, by and with the advice and consent of the Lords Spiritual and Temporal, and Commons, in this present Parliament assembled, and by the authority of the same, as follows:—

Part I Customs and Excise¶

1 Duties on spirits, beer, wine, made-wine and cider. C1¶

2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F2¶

F1133 Hydrocarbon oil, etc. ¶

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4 Aviation gasoline. C2¶

5 Vehicles excise duty: Great Britain. C3¶

F66 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .¶

7 ¶

8 Betting and gaming duties.¶

9 Immature spirits for home use and loss allowance for imported beer.¶

10 Regulator powers. C5¶

11 Power of Commissioners with respect to agricultural levies etc.¶

12 Delegation of Commissioners’ functions. C7¶

In subsection (1) of section 8 of the Customs and Excise Management Act 1979 (functions of Commissioners may be exercised by secretaries, assistant secretaries, etc.) for paragraphs (b) and (c) there shall be substituted the following paragraph:—Part II ¶

13 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F14¶

18 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F15¶

Part III Income Tax, Corporation Tax and Capital Gains Tax¶

Chapter I General¶

20 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F16¶

27 Termination of the option mortgage schemes.¶

28 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F18¶

68 Postponement of recovery of tax. C9¶

69 ¶

Chapter II ¶

70–79 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F20¶

C11Chapter III Capital Gains¶

F2180 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .¶

81 Increase of chattel exemption.¶

82 Extension of general relief for gifts.¶

F2483 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .¶

F2584 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .¶

85 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F26¶

F2786 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .¶

F2887 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .¶

F2988 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .¶

C1089 ¶

Part IV ¶

90 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F31¶

Part V Stamp Duty¶

F32128 Reduction of duty on conveyances and leases.¶

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .C13129 Exemption from duty on grants, transfers to charities, etc. C12¶

130 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F36¶

131 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F37¶

Part VI Oil Taxation¶

Chapter I General¶

132 Increase of petroleum revenue tax and ending of supplementary petroleum duty.¶

133 Export sales of gas.¶

C16134 Alternative valuation of ethane used for petrochemical purposes.¶

135 Determination of oil fields.¶

136 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F40¶

F114137 Expenditure met by regional development grants to be disregarded for certain purposes.¶

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .138 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F41¶

Chapter II Advance Petroleum Revenue Tax¶

139 Liability for APRT and credit against liability for petroleum revenue tax.¶

140 Increase of gross profit by reference to royalties in kind.¶

141 Reduction of gross profit by reference to exempt allowance.¶

142 Consequences of crediting APRT against liability for petroleum revenue tax.¶

Part VII Miscellaneous and Supplementary¶

143 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F47¶

144 ¶

145 Certificates of tax deposit: extension of interest period.¶

For the purposes of certificates of tax deposit issued by the Treasury under section 12 of the M28 National Loans Act 1968 on terms published before 31st July 1980, the date which is the due date in relation to—146 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F50¶

147 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F51¶

F52148 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .¶

149 Recovery of overpayment of tax, etc.¶

F115150 Investment in gilt-edged unit trusts. ¶

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .151 National savings accounts.¶

152 Additional power of Treasury to borrow. C18¶

153 Variable rates of interest for government lending. C19¶

154 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F55¶

155 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F56¶

F109156 Dissolution of Board of Referees.¶

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .157 Short title, interpretation, construction and repeals.¶

Schedules

F111SCHEDULE 1 ¶

Wine: Rates of Duty

Section 1(3).

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

SCHEDULE 2. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F59 ¶

F60SCHEDULE 3 ¶

I Provisions Substituted for Part II of Schedule 1¶

| Description of vehicle | Rate of duty |

|---|---|

| £ | |

| 1. Bicycles and tricycles of which the cylinder capacity of the engine does not exceed 150 cubic centimetres ... ... | 8.00 |

| 2. Bicycles of which the cylinder capacity of the engine exceeds 150 cubic centimetres but does not exceed 250 cubic centimetres; tricycles (other than those in the foregoing paragraph) and vehicles (other than mowing machines) with more than three wheels, being tricycles and vehicles neither constructed nor adapted for use nor used for the carriage of a driver or passenger ... ... ... ... | 16.00 |

| 3. Bicycles and tricycles not in the foregoing paragraphs ... | 32.00 |

II Provisions Substituted for Part II of Schedule 2¶

| Description of vehicle | Rate of duty |

|---|---|

| £ | |

| Hackney carriages ... ... | 40.00 |

| with an additional 80p for each person above 20 (excluding the driver) for which the vehicle has seating capacity. |

III Provisions Substituted for Part II of Schedule 3¶

| Weight unladen of vehicle | Rate of duty | |||

|---|---|---|---|---|

| 1. Description of vehicle | 2. Exceeding | 3. Not exceeding | 4. Initial | 5. Additional for each ton or part of a ton in excess of the weight in column 2 |

| £ | £ | |||

| 1. Agricultural machines; digging machines; mobile cranes; works trucks; mowing machines; fishermen’s tractors. | 13.50 | |||

| 2. Haulage vehicles, being showmen’s vehicles. | 7¼ tons | 130.00 | ||

| 7¼ tons | 8 tons | 156.00 | ||

| 8 tons | 10 tons | 183.00 | ||

| 10 tons | 183.00 | 28.00 | ||

| 3. Haulage vehicles, not being showmen’s vehicles. | 2 tons | 155.00 | ||

| 2 tons | 4 tons | 278.00 | ||

| 4 tons | 6 tons | 402.00 | ||

| 6 tons | 7¼ tons | 525.00 | ||

| 7¼ tons | 8 tons | 642.00 | ||

| 8 tons | 10 tons | 642.00 | 109.00 | |

| 10 tons | 860.00 | 123.00 | ||

IV Provisions Substituted for Part II of Schedule 4Tables Showing Annual Rates of Duty on Goods Vehicles¶

Table A General Rates of Duty¶

| Weight unladen of vehicle | Rate of duty | |||

|---|---|---|---|---|

| 1. Description of vehicle | 2. Exceeding | 3. Not exceeding | 4. Initial | 5. Additional for each¼ ton or part of a¼ ton in excess of the weight in column 2 |

| £ | £ | |||

| 1. Farmers’ goods vehicles ... | 12 cwt. | 46 | ||

| 12 cwt. | 16 cwt. | 50 | ||

| 16 cwt. | 1 ton | 54 | ||

| 1 ton | 3 tons | 53 | 7 | |

| 3 tons | 4 tons | 106 | 5 | |

| 4 tons | 7 tons | 126 | 4 | |

| 7 tons | 9 tons | 176 | 2 | |

| 9 tons | 233 | 6 | ||

| 2. Showmen’s goods vehicles ... | 12 cwt. | 46 | ||

| 12 cwt. | 16 cwt. | 50 | ||

| 16 cwt. | 1 ton | 54 | ||

| 1 ton | 3 tons | 53 | 7 | |

| 3 tons | 4 tons | 106 | 5 | |

| 4 tons | 6 tons | 126 | 4 | |

| 6 tons | 9 tons | 156 | 7 | |

| 9 tons | 278 | 10 | ||

| 3. Tower wagons ... ... | 12 cwt. | 62 | ||

| 12 cwt. | 16 cwt. | 69 | ||

| 16 cwt. | 1 ton | 78 | ||

| 1 ton | 4 tons | 77 | 8 | |

| 4 tons | 6 tons | 171 | 9 | |

| 6 tons | 9 tons | 242 | 8 | |

| 9 tons | 394 | 15 | ||

| 4. Goods vehicles not included in any of the foregoing provisions of this Part of this Schedule. | 1 ton | 80 | ||

| 1 ton | 1¼ tons | 90 | ||

| 1¼ tons | 1½ tons | 100 | ||

| 1½ tons | 3 tons | 130 | 22 | |

| 3 tons | 4 tons | 264 | 23 | |

| 4 tons | 9 tons | 340 | 40 | |

| 9 tons | 10 tons | 1,351 | 48 | |

| 10 tons | 1,537 | 57 | ||

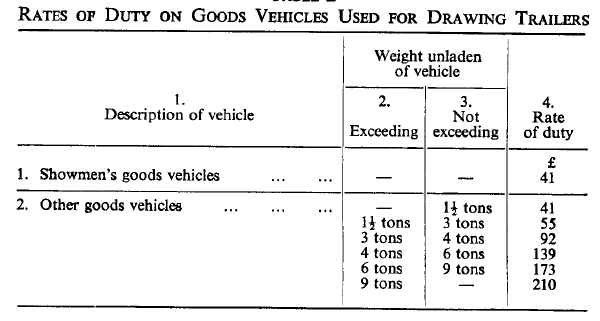

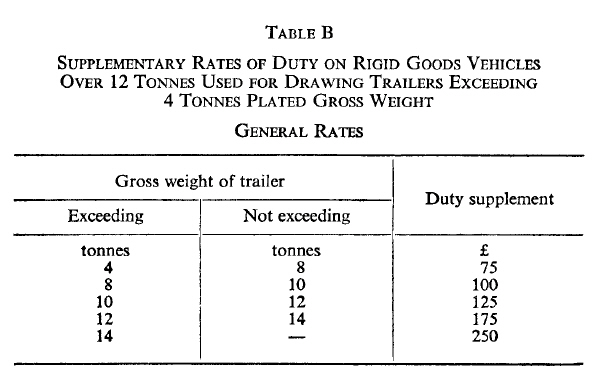

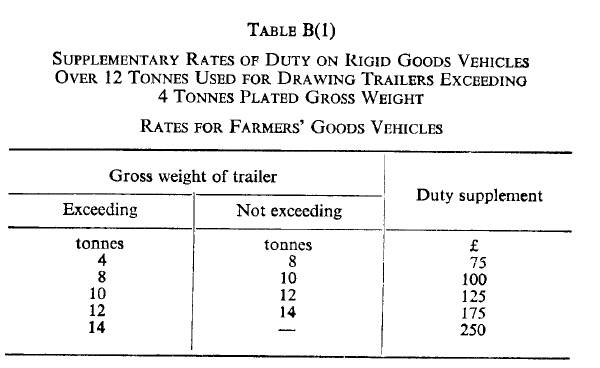

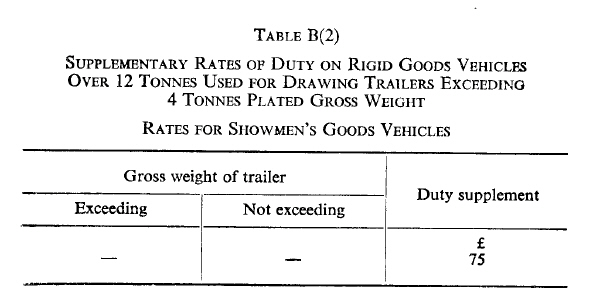

Table B Rates of Duty on Goods Vehicles Used for Drawing Trailers¶

V Provisions Substituted for Part II of Schedule 5¶

| Description of vehicle | Rate of duty |

|---|---|

| £ | |

| 1. Vehicles not exceeding seven horse-power, if registered under the Roads Act 1920 for the first time before 1st January 1947 ... ... ... ... | 57.00 |

| 2. Vehicles not included above ... ... ... ... ... | 80.00 |

F67Schedule 4 ¶

(repealed 1.10.1991) F67. . .

F61I F61. . .¶

F62II F62. . .¶

F63III F63. . .¶

F65IV F65. . .¶

Table A F64. . .¶

F66V F66. . .¶

C21Schedule 5 ¶

Annual Rates of Duty on Goods Vehicles

Sections 5(4) and 6(4).

F68Part A ¶

Part I General Provisions¶

Vehicles chargeable at the basic rate of duty¶

1 ¶

Vehicles exceeding 7.5 but not exceeding 12 tonnes plated weight¶

2 ¶

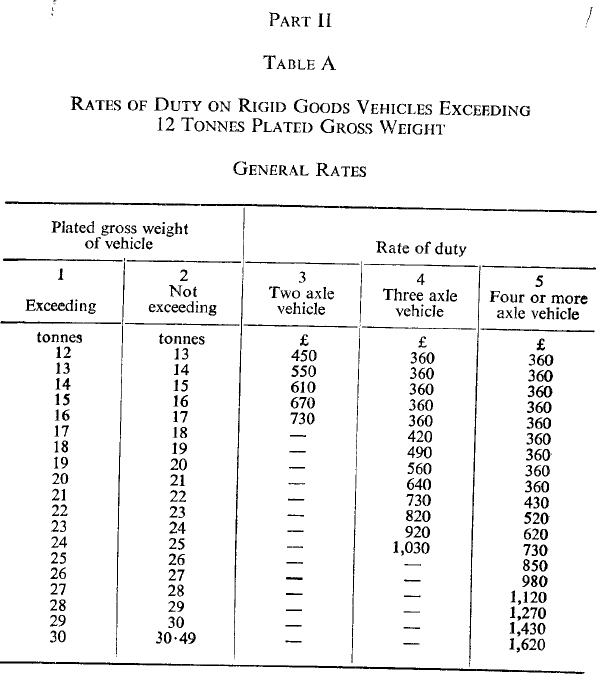

Subject to paragraphs 1(1)(c) above and 6 below, the annual rate of duty applicable to a goods vehicle which has a plated gross weight or a plated train weight which exceeds 7.5 tonnes but does not exceed 12 tonnes shall be £360.Rigid goods vehicles exceeding 12 tonnes plated gross weight¶

3 ¶

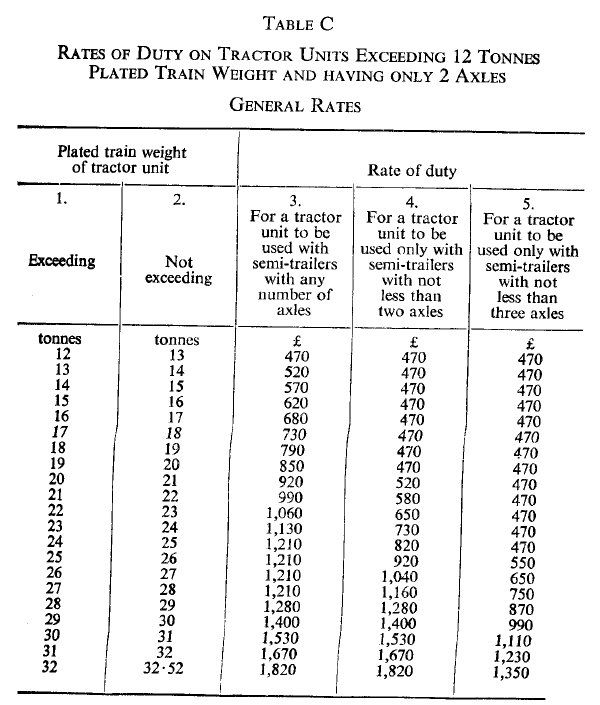

Tractor units exceeding 12 tonnes plated train weight¶

4 ¶

Special types of vehicles¶

5 ¶

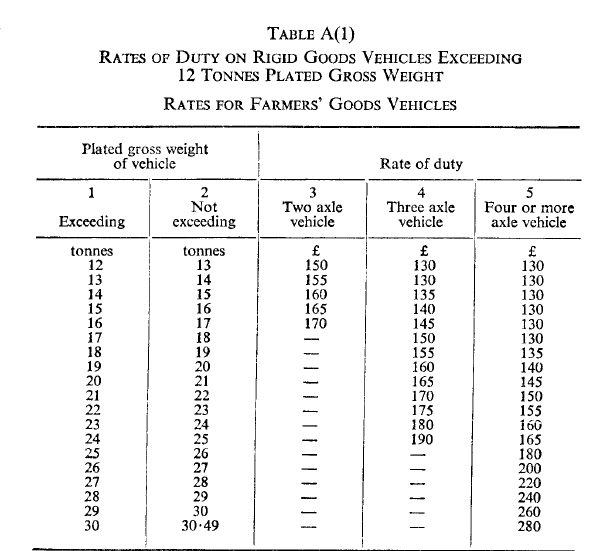

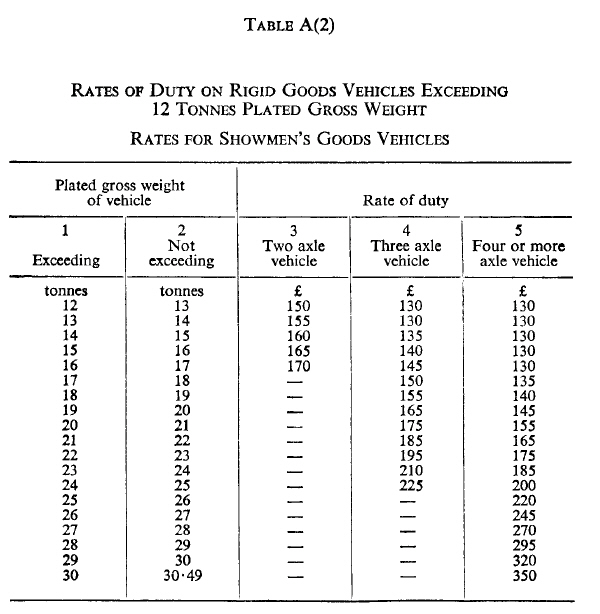

Farmer’s goods vehicles and showmen’s goods vehicles¶

6 ¶

Smaller goods vehicles¶

7 ¶

If a goods vehicle—Vehicles treated as having reduced plated weights¶

8 ¶

Plated and unladen weights¶

9 ¶

Goods vehicles used partly for private purposes¶

10 ¶

Exempted vehicles¶

11 ¶

Duty shall not be chargeable by virtue of this Schedule in respect of—12 ¶

13 ¶

Tractor units used with semi-trailers having only one axle when duty paid by reference to use with semi-trailers having more than one axle¶

14 ¶

Interpretation¶

15 ¶

- “agricultural machine” has the same meaning as in Schedule 3 to this Act;

- “axle” includes—

- “basic rate of duty” has the meaning given by paragraph 1(2);

- “business” includes the performance by a local or public authority of its functions;

- “farmer’s goods vehicle” means, subject to paragraph 10(2) above, a goods vehicle registered under this Act in the name of a person engaged in agriculture and used on public roads solely by him for the purpose of the conveyance of the produce of, or of articles required for the purposes of, the agricultural land which he occupies, and for no other purposes;

- “fishermen’s tractor” has the same meaning as in Schedule 3 to this Act;

- “goods vehicle” means a mechanically propelled vehicle (including a tricycle as defined in Schedule 1 to this Act and weighing more than 425 kilograms unladen) constructed or adapted for use and used for the conveyance of goods or burden of any description, whether in the course of trade or otherwise;

- “mobile crane” has the same meaning as in Schedule 3 to this Act;

- “rigid goods vehicle” means a goods vehicle which is not a tractor unit;

- “showman’s goods vehicle” means a showman’s vehicle which is a goods vehicle and is permanently fitted with a living van or some other special type of body or superstructure, forming part of the equipment of the show of the person in whose name the vehicle is registered under this Act;

- “showman’s vehicle” has the same meaning as in Schedule 3 to this Act;

- “stub axle” means an axle on which only one wheel is mounted;

- “tower wagon” means a goods vehicle—

- “tractor unit” means a goods vehicle to which a semi-trailer may be so attached that part of the semi-trailer is super-imposed on part of the goods vehicle and that when the semi-trailer is uniformly loaded not less than 20 per cent. of the weight of its load is borne by the goods vehicle;

- “trailer” shall be construed in accordance with sub-paragraph (2) below;

- “unladen weight” has the same meaning as it has for the purposes of the M56Road Traffic Act 1972 by virtue of section 194 of that Act; and

- “works truck” has the same meaning as in Schedule 3 to this Act.

F70Part B F70. . .¶

C22Schedule 6 ¶

Betting and Gaming Duties

Section 8.

Part I General¶

Part II ¶

Part III Gaming Licence Duty¶

F148Part IV Bingo Duty¶

Part V Gaming Machine Licence Duty¶

Great Britain¶

Schedules 7—10. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F79 ¶

Schedules 11, 12. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F80 ¶

F95Schedule 13 ¶

F89Part I ¶

Part disposals¶

Disposals on a no-gain/no-loss basis¶

F84 Subsequent disposals following no-gain/no-loss disposals¶

Receipts etc. which are not treated as disposals but affect relevant allowable expenditure¶

Reorganisations, reconstructions etc.¶

Options¶

F94Part II ¶

Schedules 14—17. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F96 ¶

C23SCHEDULE 18 ¶

Alternative Valuation of Ethane Used for Petrochemical Purposes

Section 134.

The election¶

Conditions for acceptance of an election¶

Notice of acceptance or rejection¶

Market value ceasing to be readily ascertainable¶

Price formula ceasing to give realistic market values¶

Acceptance or rejection of new price formula¶

Returns¶

Penalties for incorrect information etc.¶

Interpretation¶

Schedule 19 ¶

Supplementary Provisions Relating to APRT

Section 139(6).

Part I Collection of Tax¶

Payment of tax¶

Assessments and appeals¶

Overpayment of tax¶

Interest¶

Transitional provisions¶

Part II Miscellaneous¶

Repayment of APRT¶

Transfer of interest in fields¶

Net profit periods¶

Abandoned fields¶

Part III Amendments¶

C29Schedule 20 ¶

National Savings Accounts

Section 151.

SCHEDULE 21. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F107 ¶

SCHEDULE 22 ¶

Repeals

Section 157.

C30Part I Miscellaneous Customs and Excise and Value Added Tax¶

| Chapter | Short title | Extent of repeal |

|---|---|---|

| 1981 c. 35. | The Finance Act 1981. | In section 1, subsections (1), (3) and (4). |

| Section 2. | ||

| In section 12, subsections (1) and (2). | ||

| Schedules 1 and 2. |

C31Part II Vehicles Excise Duty¶

| Chapter | Short title | Extent of repeal |

|---|---|---|

| 1971 c. 10. | The Vehicles (Excise) Act 1971. | In Schedule 6, paragraphs 3 and 5. |

| 1972 c. 10 (N.I.). | The Vehicles (Excise) Act (Northern Ireland) 1972. | In Schedule 7, paragraphs 3 and 5. |

| 1981 c. 56. | The Transport Act 1981. | Section 33. |

| Section 34. | ||

| Schedule 11. | ||

| 1981 c. 35. | The Finance Act 1981. | In section 7, subsections (2) and (3). |

| In section 8, subsections (2) and (3). | ||

| Schedule 3. | ||

| Schedule 4. |

The repeals in the Finance Act 1981 do not affect licences taken out before 10th March 1982.

C32Part III Gaming Machine Licence Duty¶

| Chapter | Short title | Extent of repeal |

|---|---|---|

| 1972 c. 11 (N.I.). | The Miscellaneous Transferred Excise Duties Act (Northern Ireland) 1972. | In section 44, subsections (3)(c) and (6)(aa). |

| In paragraph 13 of Schedule 3 the words “the peak rate”. | ||

| 1980 c. 48. | The Finance Act 1980. | In Schedule 6, paragraph 15(2) and (4). |

| 1981 c. 35. | The Finance Act 1981. | Section 9(6). |

| 1981 c. 63. | The Betting and Gaming Duties Act 1981. | In section 22, subsections (5)(c) and (6). |

| In section 25(4), the word “and”, at the end of paragraph (b), and paragraph (c). |

These repeals do not affect licences for periods beginning before 1st October 1982.

C33Part IV Income and Corporation Tax: General¶

| Chapter | Short title | Extent of repeal |

|---|---|---|

| 1970 c. 10. | The Income and Corporation Taxes Act 1970. | Section 8(2)(b)(ii). |

| Section 131(6). | ||

| Section 228(5). | ||

| Section 249(5). | ||

| Section 416(4). | ||

| 1975 c. 45. | The Finance (No. 2) Act 1975. | Section 36(5)(a). |

| In section 36A(1), paragraph (a) and, in paragraph (b), the words “(including any interest paid in connection therewith)”. | ||

| 1976 c. 40. | The Finance Act 1976. | Section 64A(7) and (8). |

| 1980 c. 48. | The Finance Act 1980. | In Schedule 12, in paragraph 7(3) the words from “and a television set” onwards. |

| 1981 c. 35. | The Finance Act 1981. | Section 24. |

| In section 27(3), the words “(except so far as made by virtue of section 4 of that Act)”. | ||

| In section 27(8) the word “and” where it appears at the end of paragraph (b). | ||

| Section 42(2)(c). | ||

| In section 68, subsections (2), (4) and (5). |

Part V Option Mortgage Schemes¶

| Chapter or number | Short title | Extent of repeal |

|---|---|---|

| 1967 c. 29. | The Housing Subsidies Act 1967. | Sections 24 to 32. |

| 1969 c. 33. | The Housing Act 1969. | Sections 78 and 79. |

| 1970 c. 10. | The Income and Corporation Taxes Act 1970. | In Schedule 15, the entry in Part II relating to the Housing Subsidies Act 1967. |

| 1971 c. 68. | The Finance Act 1971. | Section 66. |

| 1974 c. 44. | The Housing Act 1974. | Section 119. |

| Schedule 11. | ||

| 1980 c. 51. | The Housing Act 1980. | Sections 114 to 116. |

| Schedule 14. | ||

| S.I. 1981/156 (N.I. 3). | The Housing (Northern Ireland) Order 1981. | Articles 141 to 152. |

These repeals have effect on 1st April 1983, but subject to subsections (2) to (4) of section 27 of this Act.

Part VI Capital Gains¶

| Chapter | Short title | Extent of repeal |

|---|---|---|

| 1979 c. 14. | The Capital Gains Tax Act 1979. | Section 55(2). |

| Section 56(2). | ||

| In section 146(3)— | ||

| the words “or 55”; | ||

| the words from “or (b)” to “paragraph 12”; | ||

| the words “or the assets are so held”; | ||

| the words from “or of the assets” to “(b) above”; | ||

| the words “and 55”. | ||

| In section 147(3), the words “or 55(1)”. | ||

| In Schedule 4— | ||

| in paragraph 2(1) the words “or 55(1)”; | ||

| paragraph 2(3)(b); | ||

| in paragraph 3(1)(a), the words “or 55(1)”. | ||

| 1980 c. 48. | The Finance Act 1980. | In section 79(4), the words from “or” onwards. |

| In section 79(5), the words from “and where” onwards. | ||

| 1981 c. 35. | The Finance Act 1981. | Section 78(1) and (3). |

The repeals of section 55(2) and 56(2) of the Capital Gains Tax Act 1979 have effect in relation to interests terminating after 5th April 1982 and the remaining repeals have effect in relation to disposals after that date.

C34Part VII Capital Transfer Tax¶

| Chapter | Short title | Extent of repeal |

|---|---|---|

| 1975 c. 7. | The Finance Act 1975. | In section 20(7) the words “(within the meaning of Schedule 5 to this Act)”. |

| Section 26(2A). | ||

| In section 51, in subsection (1) the definition of “capital distribution”, and in subsection (5) the words “(except paragraph 11(10) of Schedule 5)”. | ||

| In Schedule 4, in paragraphs 2(7), 12(4) and 19(1)(c) the words “or section 89 of the Finance Act 1980” and the words “or paragraph 3 of Schedule 15 to the Finance Act 1981”. | ||

| In Schedule 5— | ||

| paragraphs 6 to 15; | ||

| paragraph 16(5); | ||

| in paragraph 17, in sub-paragraph (1) the words “or (c) charities”, sub-paragraph (3)(c) to (e) and the word “and” immediately preceding paragraph (c), and sub-paragraphs (4) and (5) to (9); | ||

| in paragraph 18 (as it applies where the failure or determination of the trusts concerned was before 12th April 1978), sub-paragraphs (2) and (3); | ||

| in paragraph 19 (as it apples to property transferred into settlement before 10th March 1981), sub-paragraphs (2) and (3); | ||

| paragraphs 20 and 21; | ||

| in paragraph 24, sub-paragraph (4). | ||

| In Schedule 6, paragraphs 10(2), 11(1A), 12(2), 13(1A) and 15(6). | ||

| 1976 c. 40. | The Finance Act 1976. | Section 79(2), (5) and (6). |

| Section 84. | ||

| In section 105, in subsection (1) the words “(2) and” and “paragraph 6(7) were omitted and”, and subsection (2). | ||

| Section 106. | ||

| Section 107(3) and (4). | ||

| Section 110(3). | ||

| In section 111, subsections (1) to (3), in subsection (4) the words from “after sub-paragraph (1)” to “Schedule 5 to this Act”, and subsection (5). | ||

| In section 118(2) the words from “and subsection (4)” onwards. | ||

| Section 118(4). | ||

| In Schedule 11, paragraph 4. | ||

| In Schedule 14, paragraphs 2, 3, 8, 11, 12, 13(c) and (d), 14, 15, 16 and 17. | ||

| 1977 c. 36. | The Finance Act 1977. | Section 50. |

| In section 51, subsections (3) and (4). | ||

| 1978 c. 42. | The Finance Act 1978. | In section 64, subsection (6), and in subsection (7) the words from the beginning to “and” and the word “other”. |

| In section 69, subsections (2) and (3), and in subsection (6) the words “6(6B) and 14(5)”. | ||

| Section 70. | ||

| In section 71(2) the words from “but” to the end. | ||

| In section 72(2) the words from “and” onwards. | ||

| In Schedule 11, paragraph 1. | ||

| 1979 c. 47. | The Finance (No. 2) Act 1979. | Section 23. |

| 1980 c. 48. | The Finance Act 1980. | In section 86, subsection (4), and in subsection (5) the words “and (4)”. |

| Section 88(1) to (6). | ||

| Sections 89 to 91. | ||

| In Schedule 15, paragraphs 3 and 4A, and in paragraph 5 the words “or 81(4)(b)”, “or a settlement which ceased to exist” and “or when the settlement ceased to exist”. | ||

| Schedule 16. | ||

| 1981 c. 35. | The Finance Act 1981. | In section 92, subsection (3), in subsection (4) the words “or 81(4)(b),”, “or a settlement which ceased to exist” and “or when the settlement ceased to exist”, and subsection (5). |

| Section 99. | ||

| Section 102. | ||

| Schedule 15. |

C35Part VIII Stamp Duty¶

| Chapter | Short title | Extent of repeal |

|---|---|---|

| 1974 c. 30. | The Finance Act 1974. | In section 49, subsections (2) and (3). |

| 1980 c. 48. | The Finance Act 1980. | In section 118(3) the words “section 49(2) of the Finance Act 1974 (relief from stamp)”. |

Part IX Oil Taxation¶

| Chapter | Short title | Extent of repeal |

|---|---|---|

| 1975 c. 22. | The Oil Taxation Act 1975. | In section 12(3) the words from “as regards” to “any oil field”. |

| In Schedule 3, in paragraph 8(1) the words from “unless it is so met by a grant” onwards. | ||

| 1980 c. 48. | The Finance Act 1980. | Section 105. |

| 1981 c. 35. | The Finance Act 1981. | Sections 122 to 128. |

| Schedule 16. |

C36Part X Board of Referees¶

| Chapter | Short title | Extent of repeal |

|---|---|---|

| 1970 c. 9. | The Taxes Management Act 1970. | Section 6(1)(b). |

| In Schedule 4, paragraph 8. | ||

| 1971 c. 62. | The Tribunals and Inquiries Act 1971. | In Schedule 1, paragraph 29(c). |

| 1975 c. 24. | The House of Commons Disqualification Act 1975. | In Schedule 1, in Part III, the entry relating to the Board of Referees appointed for the purposes of section 26 of the Capital Allowances Act 1968. |

| 1975 c. 25. | The Northern Ireland Assembly Disqualification Act 1975. | In Schedule 1, in Part III, the entry relating to the Board of Referees appointed for the purposes of section 26 of the Capital Allowances Act 1968. |

C37Part XI Spent Enactments¶

| Chapter | Short title | Extent of repeal |

|---|---|---|

| 1947 c. 46. | The Wellington Museum Act 1947. | Section 4(3). |

| 1970 c. 10. | The Income and Corporation Taxes Act 1970. | Section 10. |

| Section 11(1), (2), (3) and (6). | ||

| In section 39(1)(d) the words “relief in respect of a child under section 10(1)(b) or” and the word “child” in the second place where it occurs. | ||

| 1971 c. 68. | The Finance Act 1971. | In Schedule 4, paragraph 3(1)(a). |

| In Schedule 6, paragraph 6. | ||

| 1975 c. 7. | The Finance Act 1975. | In Schedule 6, paragraphs 1(3) and (4) and 10(4) and (5). |

| 1975 c. 45. | The Finance (No. 2) Act 1975. | In Schedule 12— |

| paragraph 5 of Part I; | ||

| paragraph 3 of Part III; | ||

| paragraph 4 of Part IV. | ||

| 1976 c. 40. | The Finance Act 1976. | Section 29(3). |

| 1977 c. 36. | The Finance Act 1977. | Section 25. |

| 1978 c. 42. | The Finance Act 1978. | Section 20(3) and (5). |

| 1979 c. 25. | The Finance Act 1979. | Section 1(4). |

| 1980 c. 48. | The Finance Act 1980. | Section 25. |

Footnotes

- X1General amendments to Tax Acts, Income Tax Acts, and/or Corporation Tax Acts made by legislation after 1.2.1991 are noted against Income and Corporation Taxes Act 1988 (c. 1, SIF 63:1) but not against each Act

- I1Act partly in force at Royal Assent, partly retrospective; all provisions so far as unrepealed fully in force at 1.2.1991. Some sections came into force at specific times of the day.

- X2The text of ss. 1–4, 9–12, Schs. 1, 2, 22 Pts. I, II was taken from S.I.F. Group 40:1 (Customs and Excise: Customs and Excise Duties), ss. 5–7, Schs. 3–5 from S.I.F. Group 107:2 (Road Traffic: Vehicle Excise Duty), s. 8, Schs. 6, 22 Pt. III from S.I.F. Group 12:2 (Betting, Gaming and Lotteries: Betting and Gaming Duties), ss. 20–79, 132–142, 146, 149–151, 156, 157(5)(7), Schs. 7–12, 18–21, 22 Pts. IV, V, IX–XI from S.I.F. Group 63:1 (Income, Corporation and Capital Gains Taxes: Income and Corporation Taxes), ss. 80–89, 148, Schs. 13, 22 Pt. VI from S.I.F. Group 63:2 (Income, Corporation and Capital Gains Taxes: Capital Gains Tax), ss. 128–131, Sch. 22 Pt. VIII from S.I.F. Group 114 (Stamp Duty), ss. 145, 152–154 from S.I.F. Group 99:3 (Public Finance and Economic Controls: National Debt), Sch. 22 Pt. VII from S.I.F. Group 65 (Inheritance Tax), s. 144 from S.I.F Group 96 (Posts and Telecommunications), s. 157(2)(3) appeared in both S.I.F. sub-groups 63:1 and 63:2, s. 157(6) appeared in S.I.F. Groups 40:1, 12:2, 63:1 and 2, 114, 65 and s. 157(1) appeared in all S.I.F. Groups previously listed; provisions omitted from S.I.F. have been dealt with as referred to in other commentary

- C1Part of the text of s. 1 is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and, except as specified, does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- M11979 c. 4

- F1S. 1(4) repealed by Finance Act 1984 (c. 43, SIF 40:1), s. 128(6), Sch. 23 Pt. I

- F2S. 2 repealed by Finance Act 1984 (c. 43, SIF 40:1), s. 128(6), Sch. 23 Pt. IV

- C2Part of the text of ss. 3 and 4 is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- M21979 c. 5.

- C3Part of the text of ss. 5 and 6 is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and, except as specified, does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- F3S. 5(1)-(4) and (7) repealed (1.9.1994) by 1994 c. 22, ss. 65, 66(1), Sch. 5 Pt. I (with s. 57(4))

- F4S. 5(5) repealed by Finance Act 1988 (c. 39, SIF 107:2), s. 148, Sch. 14 Pt. II

- F5Ss. 5(6) and 6(7) deemed partly repealed retrospectively (20.3.1991) for a specified purpose and repealed fully (25.7.1991) by Finance Act 1991 (c. 31, SIF 107:2), s. 123, Sch. 19 Pt. III, Note 3

- F6S. 6 repealed(1.10.1991) by Finance Act 1991 (c. 31, SIF 107:2), ss. 10, 123, Sch. 19 Pt.IV; S.I. 1991/2021, art.2.

- F7S. 7(1) and (3) repealed (1.9.1994) by 1994 c. 22, ss. 65, 66(1), Sch. 5 Pt. I (with s. 57(4))

- F8S. 7(2)(4) repealed(1.10.1991) by Finance Act 1991 (c. 31, SIF 107:2), ss. 10, 123, Sch. 19 Pt. IV, Note; S.I. 1991/2021, art. 2.

- F9S. 8(1)(a) repealed by Finance Act 1990 (c. 29, SIF 12:2), s. 132, Sch. 19 Pt. I

- F10S. 9(1)(2) repealed by Finance Act 1990 (c. 29, SIF 40:1), s. 132, Sch. 19 Pt. I

- C4The text of ss. 9(3), 10, 11(2)(3), 12 is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- C5The text of ss. 9(3), 10, 11(2)(3), 12 is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- M31979 c. 8.

- M41972 c. 68.

- F11Words in s. 11(1)(a) substituted (15.11.2001) by S.I. 2001/3686, reg. 6(9)(a)(i)

- F12Words in s. 11(1)(b) substituted (15.11.2001) by S.I. 2001/3686, reg. 6(9)(a)(ii)

- M51968 c. 60.

- M61978 c. 31.

- M71969 c. 16 (N.I.).

- C6The text of ss. 9(3), 10, 11(2)(3), 12 is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- M81979 c. 2.

- F13S. 11(3) repealed (15.11.2001) by S.I. 2001/3686, reg. 6(9)(b)

- C7The text of ss. 9(3), 10, 11(2)(3), 12 is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- F14Ss. 13–17 repealed by Value Added Tax Act 1983 (c. 55), s. 50(2), Sch. 11

- F15Ss. 18 and 19 repealed by Car Tax Act 1983 (c. 53), s. 10(4), Sch. 3

- F16Ss. 20–26 repealed by Income and Corporation Taxes Act 1988 (c. 1, SIF 63:1), s. 844 and Sch. 31

- F17Words substituted by Income and Corporation Taxes Act 1988 (c. 1, SIF 63:1), Sch. 29 para. 32

- C8See Income and Corporation Taxes Act 1988 (c. 1, SIF 63:1), s. 370(3)(a)

- M91967 c. 29.

- M10S.I. 1981/156 (N.I. 3).

- F18Ss. 28–67 repealed by Income and Corporation Taxes Act 1988 (c. 1, SIF 63:1), s. 844 and Sch. 31 (and see Finance Act 1988 (c. 39, SIF 63:1, 2), s. 148 and Sch. 14 Pt. VI for partial repeal of s. 41 in relation to acquisitions on or after 26 October 1987)

- C9Part of the text of s. 68 is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- M111970 c. 9.

- F19S. 69 repealed by Finance Act 1989 (c. 26), s. 187 and Sch. 17 Pt. VIII in relation to tax charged by any assessment notice of which is issued after 30 July 1982

- F20Ss. 70–79 repealed by Capital Allowances Act 1990 (c. 1, SIF 63:1), s. 164(4) and Sch. 2

- F21S. 80 repealed (6.3.1992 with effect as mentioned in s. 289(1)(2) of the repealing Act) by Taxation of Chargeable Gains Act 1992 (c. 12), ss. 289, 290, Sch.12 (with s. 201(3), Sch. 11 paras. 20, 22, 26(2), 27

- F22S. 81 repealed by Finance Act 1989 (c. 26), s. 187 and Sch. 17 Pt. VII in relation to disposals on or after 6 April 1989 (and s. 81(1)(b) repealed in relation to assets acquired on or after 6 April 1989)

- M121970 c. 9.

- F23S. 82 repealed by Finance Act 1989 (c. 26), s. 187 and Sch. 17 Pt. VII in relation to disposals on or after 14 March 1989 (except where relief given under Finance Act 1980 (c. 48) s. 79 in respect of a disposal made on or after that date)

- M131980 c. 48.

- M141981 c. 35.

- F24Ss. 83-88 repealed (6.3.1992 with effect as mentioned in s. 289(1)(2) of the repealing Act) by Taxation of Chargeable Gains Act 1992 (c. 12), ss. 289, 290, Sch.12 (with s. 201(3), Sch. 11 paras. 20, 22, 26(2), 27)

- F25Ss. 83-88 repealed (6.3.1992 with effect as mentioned in s. 289(1)(2) of the repealing Act) by Taxation of Chargeable Gains Act 1992 (c. 12), ss. 289, 290, Sch.12 (with s. 201(3), Sch. 11 paras. 20, 22, 26(2), 27)

- F26S. 85 repealed by Finance Act 1984 (c. 43, SIF 40:1), s. 128(6), Sch. 23 Pt. VIII for disposals on or after 6 April 1984; Ss. 83-88 repealed (6.3.1992 with effect as mentioned in s. 289(1)(2) of the repealing Act) by Taxation of Chargeable Gains Act 1992 (c. 12), ss. 289, 290, Sch.12 (with s. 201(3), Sch. 11 paras. 20, 22, 26(2), 27)

- F27Ss. 83-88 repealed (6.3.1992 with effect as mentioned in s. 289(1)(2) of the repealing Act) by Taxation of Chargeable Gains Act 1992 (c. 12), ss. 289, 290, Sch.12 (with s. 201(3), Sch. 11 paras. 20, 22, 26(2), 27)

- F28Ss. 83-88 repealed (6.3.1992 with effect as mentioned in s. 289(1)(2) of the repealing Act) by Taxation of Chargeable Gains Act 1992 (c. 12), ss. 289, 290, Sch.12 (with s. 201(3), Sch. 11 paras. 20, 22, 26(2), 27)

- F29Ss. 83-88 repealed (6.3.1992 with effect as mentioned in s. 289(1)(2) of the repealing Act) by Taxation of Chargeable Gains Act 1992 (c. 12), ss. 289, 290, Sch.12 (with s. 201(3), Sch. 11 paras. 20, 22, 26(2), 27)

- F30S. 89 repealed by Finance Act 1985 (c. 54), ss. 68, 98(6), Schs. 19 Pt. I and 27 Pt. VII for disposals made on or after 6 April 1985 or 1 April 1985 for companies, 2 July 1986 for gilt-edged securities (Capital Gains Tax Act 1979 (c. 14, SIF 63:2) Sch. 2) and qualifying corporate bonds (Finance Act 1984 (c. 43, SIF 40:1) s. 64), or 28 February 1986 for other securities within the meaning of Finance Act 1985 (c. 54) Part II Ch. IV

- C10See—Income and Corporation Taxes Act 1988 (c. 1, SIF 63:1), ss. 57, 289 and Sch. 4 para. 12Capital Gains Tax Act 1979 (c. 14, SIF 63:2), s. 149C

- C11See Income and Corporation Taxes Act 1988 (c. 1, SIF 63:1), Sch. 28 para. 2(2) re computation of offshore income gains

- F31Part IV (ss. 90–127) repealed by Capital Transfer Tax Act 1984 (c. 51), ss. 274, 277, Schs. 7, 9

- F32S. 128 repealed (27.7.1999 with effect as mentioned in Sch. 20 Pt. V(2) notes 1, 2 of the amending Act) by 1999 c. 16, s. 139, Sch. 20 Pt. V(2)

- C12S. 129 modified by Finance Act 1983 (c. 28, SIF 63:1), s. 46(3)(c)

- C13S. 129 excluded (6.5.1992) by Further and Higher Education Act 1992 (c. 13), s. 88(2); S.I. 1992/831, art. 2, Sch. 1

- F33Words in s. 129(1) inserted (2.7.1998) by 1998 c. 22, ss. 24(4), 27(4)

- F34Words in s. 129(1) substituted for S. 129(1)(a) and the preceding words “by virtue of” (27.7.1999 with effect in relation to instruments executed on or after 1.10.1999) by 1999 c. 16, s. 112(4)(6), Sch. 14 para. 7

- F35S. 129(1)(b) repealed by Finance Act 1985 (c. 54, SIF 114), s. 98(6), Sch. 27 Pt. IX(1)

- M151891 c. 39.

- F36S. 130 repealed by Finance Act 1989 (c. 26, SIF 114), s. 187(1), Sch. 17 Pt. IX

- F37S. 131 repealed by Capital Transfer Tax Act 1984 (c. 51, SIF 65), s. 277, Sch. 9

- C14Part of the text of ss. 132(2), 133(1) is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- M161981 c. 35.

- C15Part of the text of ss. 132(2), 133(1) is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- M171981 c. 35.

- C16S. 134 restricted (3.5.1994) by 1994 c. 9, s. 236(3)

- F38Words inserted by Income and Corporation Taxes Act 1988 (c. 1, SIF 63:1), Sch. 29 para. 29

- F39Words in s. 134(2) inserted (3.5.1994) by 1994 c. 9, s. 236(3)(a)

- M181981 c. 35.

- M191981 c. 35.

- M201970 c. 9.

- M211980 c. 48.

- M221981 c. 35.

- M231980 c. 48.

- M241980 c. 1.

- F40S. 136 repealed by Income and Corporation Taxes 1988 (c. 1, SIF 63:1), s. 844 and Sch. 31

- F41S. 138 repealed by Income and Corporation Taxes 1988 (c. 1, SIF 63:1), s. 844 and Sch. 31

- F42Words inserted by Finance Act 1983 (c. 28), s. 35(1)

- F43Words substituted by Finance Act 1983 (c. 28), s. 35(1)

- F44S. 139(2)(a)–(d) substituted for words by Finance Act 1983 (c. 28), s. 35(2)

- F45Words substituted by Finance Act 1983 (c. 28), s. 35(3)

- M251968 c. 2.

- M261980 c. 48.

- M271934 c. 36.

- F46S. 142(3)(4) repealed by Finance Act 1987 (c. 16), s. 72(7) and Sch. 16 Part VII

- F47S. 143 repealed by Finance Act 1984 (c. 43), s. 128(6), Sch. 23 Pts. XI, XIV

- F48S. 144(1)(2)(4)(5) repealed by Finance Act 1989 (c. 26), s. 187(1), Sch. 17 Pt. XI

- F49S. 144(3) repealed by Broadcasting Act 1990 (c. 42), s. 203(3), Sch. 21

- M281968 c. 13.

- F50S. 146 repealed by Oil and Pipelines Act 1985 (c. 62), s. 7(4) and Sch. 4 Part I

- F51S. 147 repealed by Gas Act 1986 (c. 44), s. 67(4), Sch. 9 Pt. II

- F52S. 148 repealed (6.3.1992 with effect as mentioned in s. 289(1)(2) of the repealing Act) by Taxation of Chargeable Gains Act 1992 (c. 12), ss. 289, 290, Sch.12 (with s. 201(3), Sch. 11 paras. 20, 22, 26(2), 27)

- C17Part of the text of s. 149(1) is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- M291970 c. 9.

- M301978 c. 42.

- M311971 c. 29.

- C18The text of s. 152 is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- M321968 c. 13.

- C19The text of s. 153 is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and, except as specified, does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- F53S. 153(3) repealed by Housing (Consequential Provisions) Act 1985 (c. 71, SIF 61), s. 3, Sch. 1 Pt. I

- F54S. 153(4) repealed (21.3.1997) by 1995 c. 24, s. 13(2), SCh. 2 Pt. I; S.I. 1997/1139, art. 2

- F55S. 154 repealed by Finance Act 1984 (c. 43, SIF 99:3), s. 128(6), Sch. 23 Pt. XIV

- F56S. 155 repealed by Finance Act 1985 (c. 54), s. 98(6), Sch. 27 Pt. X Note 2

- F57S. 157(2) substituted by Income and Corporation Taxes Act 1988 (c. 1, SIF 63:1), Sch. 29 para. 32

- M331970 c. 10.

- M341979 c. 14.

- C20The text of s. 157(4) is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- M351975 c. 7.

- M361975 c. 22.

- F58Words repealed by Income and Corporation Taxes 1988 (c. 1, SIF 63:1), s. 844 and Sch. 31

- M371947 c. 46.

- M381975 c. 45.

- F59Sch. 2 repealed by Finance Act 1984 (c. 43), s. 128(6), Sch. 23 Pt. I

- F60Sch. 3 repealed (1.9.1994) by 1994 c. 22, ss. 65, 66(1), SCh. 5 Pt. I (with s. 57(4))

- F61Sch. 4 repealed (1.10.1991) by Finance Act 1991 (c. 31, SIF 107:2), ss. 10, 123, Sch. 19 Pt.IV, Note; S.I. 1991/2021, art.2.

- F62Sch. 4 repealed (1.10.1991) by Finance Act 1991 (c. 31, SIF 107:2), ss. 10, 123, Sch. 19 Pt.IV, Note; S.I. 1991/2021, art.2.

- F63Sch. 4 repealed (1.10.1991) by Finance Act 1991 (c. 31, SIF 107:2), ss. 10, 123, Sch. 19 Pt.IV, Note; S.I. 1991/2021, art.2.

- F64Sch. 4 repealed (1.10.1991) by Finance Act 1991 (c. 31, SIF 107:2), ss. 10, 123, Sch. 19 Pt. IV, Note; S.I. 1991/2021, art. 2

- F65Sch. 4 repealed (1.10.1991) by Finance Act 1991 (c. 31, SIF 107:2), ss. 10, 123, Sch. 19 Pt.IV, Note; S.I 1991/2021, art.2.

- F66Sch. 4 repealed (1.10.1991) by Finance Act 1991 (c. 31, SIF 107:2), ss. 10, 123, Sch. 19 Pt.IV, Note; S.I. 1991/2021, art.2.

- F67Sch. 4 repealed (1.10.1991) by Finance Act 1991 (c. 31, SIF 107:2), ss. 10, 123, Sch. 19 Pt.IV, Note; S.I. 1991/2021, art.2.

- F68Sch. 5 Pt. A repealed (1.9.1994) by 1994 c. 22, ss. 65, 66(1), SCh. 5 Pt. I (with s. 57(4))

- F69Sch. 5 Pt. B repealed(1.10.1991) by Finance Act 1991 (c. 31, SIF 107:2), ss. 10, 123, Sch. 19 Pt.IV, Note; S.I. 1991/2021, art.2.

- F70Sch. 5 Pt. B repealed(1.10.1991) by Finance Act 1991 (c. 31, SIF 107:2), ss. 10, 123, Sch. 19 Pt.IV, Note; S.I. 1991/2021, art.2.

- C21The text of Sch. 5 is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and, except as specified, does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- M391981 c. 63.

- M401972 c. 11 (N.I.).

- F71Sch. 6 para. 2 repealed by Finance Act 1990 (c. 29, SIF 12:2), s. 132, Sch. 19 Pt. I

- F72Sch. 6 paras. 6–8 repealed by Finance Act 1984 (c. 43, SIF 12:2), s. 128(6), Sch. 23 Pt. II

- F73Sch. 6 para. 9 repealed (3.5.1994) by 1994 c. 9, ss. 6, 258, Sch. 3, Sch. 26 Pt. II

- F74Sch. 6 para. 10 repealed by Finance Act 1987 (c. 16, SIF 12:2), s. 72(7), Sch. 16 Part II Note 2

- F75Sch. 6 para. 11 repealed (3.5.1994) by 1994 c. 9, ss. 6, 258, Sch. 3, Sch. 26 Pt. II

- F76Sch. 6 para. 15 repealed (3.5.1994) by 1994 c. 9, ss. 6, 258, Sch. 3, Sch. 26 Pt. II

- F77Sch. 6 para. 16 repealed by Finance Act 1984 (c. 43, SIF 12:2), s. 128(6), Sch. 23 Pt. II

- F78Sch. 6 paras. 18–24 repealed by Finance Act 1985 (c. 54, SIF 12:2), s. 77, Sch. 27 Pt. III Note 1

- C22Part of the text of Sch. 6 is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and, except as specified, does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- F79Schs. 7–10 repealed by Income and Corporation Taxes Act 1988 (c. 1), s. 844, Sch. 31

- F80Schs. 11, 12 repealed by Capital Allowances Act 1990 (c. 1, SIF 63:1), s. 164(4) and Sch. 2

- F81Schedule 13 repealed (6.3.1992 with effect as mentioned in s. 289(1)(2) of the repealing Act) by Taxation of Chargeable Gains Act 1992 (c. 12), ss. 289, 290, Sch.12 (with s. 201(3), Sch. 11 paras. 20, 22, 26(2), 27)

- F82Schedule 13 repealed (6.3.1992 with effect as mentioned in s. 289(1)(2) of the repealing Act) by Taxation of Chargeable Gains Act 1992 (c. 12), ss. 289, 290, Sch. 12 (with s. 201(3), Sch. 11 paras. 20, 22, 26(2), 27)

- F83Schedule 13 repealed (6.3.1992 with effect as mentioned in s. 289(1)(2) of the repealing Act) by Taxation of Chargeable Gains Act 1992 (c. 12), ss. 289, 290, Sch.12 (with s. 201(3), Sch. 11 paras. 20, 22, 26(2), 27)

- F84Sch. 13 para. 3 repealed by Finance Act 1985 (c. 54), ss. 68, 98(6), Schs. 19 Pt. I and 27 Pt. VII for disposals made on or after 6 April 1985 or 1 April 1985 for companies, 2 July 1986 for gilt-edged securities (Capital Gains Tax Act 1979 (c. 14, SIF 63:2) Sch. 2) and qualifying corporate bonds (Finance Act 1984 (c. 43, SIF 40:1) s. 64), or 28 February 1986 for other securities within the meaning of Finance Act 1985 (c. 54) Part II Ch. IV

- F85Schedule 13 repealed (6.3.1992 with effect as mentioned in s. 289(1)(2) of the repealing Act) by Taxation of Chargeable Gains Act 1992 (c. 12), ss. 289, 290, Sch. 12 (with s. 201(3), Sch. 11 paras. 20, 22, 26(2), 27)

- F86Schedule 13 repealed (6.3.1992 with effect as mentioned in s. 289(1)(2) of the repealing Act) by Taxation of Chargeable Gains Act 1992 (c. 12), ss. 289, 290, Sch.12 (with s. 201(3), Sch. 11 paras. 20, 22, 26(2), 27)

- F87Schedule 13 repealed (6.3.1992 with effect as mentioned in s. 289(1)(2) of the repealing Act) by Taxation of Chargeable Gains Act 1992 (c. 12), ss. 289, 290, Sch. 12 (with s. 201(3), Sch. 11 paras. 20, 22, 26(2), 27)

- F88Schedule 13 repealed (6.3.1992 with effect as mentioned in s. 289(1)(2) of the repealing Act) by Taxation of Chargeable Gains Act 1992 (c. 12), ss. 289, 290, Sch.12 (with s. 201(3), Sch. 11 paras. 20, 22, 26(2), 27)

- F89Schedule 13 repealed (6.3.1992 with effect as mentioned in s. 289(1)(2) of the repealing Act) by Taxation of Chargeable Gains Act 1992 (c. 12), ss. 289, 290, Sch.12 (with s. 201(3), Sch. 11 paras. 20, 22, 26(2), 27)

- F90Schedule 13 repealed (6.3.1992 with effect as mentioned in s. 289(1)(2) of the repealing Act) by Taxation of Chargeable Gains Act 1992 (c. 12), ss. 289, 290, Sch. 12 (with s. 201(3), Sch. 11 paras. 20, 22, 26(2), 27)

- F91Schedule 13 repealed (6.3.1992 with effect as mentioned in s. 289(1)(2) of the repealing Act) by Taxation of Chargeable Gains Act 1992 (c. 12), ss. 289, 290, Sch.12 (with s. 201(3), Sch. 11 paras. 20, 22, 26(2), 27)

- F92Schedule 13 repealed (6.3.1992 with effect as mentioned in s. 289(1)(2) of the repealing Act) by Taxation of Chargeable Gains Act 1992 (c. 12), ss. 289, 290, Sch. 12 (with s. 201(3), Sch. 11 paras. 20, 22, 26(2), 27)

- F93Schedule 13 repealed (6.3.1992 with effect as mentioned in s. 289(1)(2) of the repealing Act) by Taxation of Chargeable Gains Act 1992 (c. 12), ss. 289, 290, Sch. 12 (with s. 201(3), Sch. 11 paras. 20, 22, 26(2), 27)

- F94Schedule 13 repealed (6.3.1992 with effect as mentioned in s. 289(1)(2) of the repealing Act) by Taxation of Chargeable Gains Act 1992 (c. 12), ss. 289, 290, Sch.12 (with s. 201(3), Sch. 11 paras. 20, 22, 26(2), 27)

- F95Schedule 13 repealed (6.3.1992 with effect as mentioned in s. 289(1)(2) of the repealing Act) by Taxation of Chargeable Gains Act 1992 (c. 12), ss. 289, 290, Sch.12 (with s. 201(3), Sch. 11 paras. 20, 22, 26(2), 27)

- F96Schs. 14–17 repealed by Capital Transfer Tax Act 1984 (c. 51), ss. 274, 277, Schs. 7, 9

- F97Words in Sch. 18 para. 3(2)(a) inserted (16.7.1992) by Finance (No. 2) Act 1992 (c. 48), s. 74, Sch. 15 para.5

- C23See Finance Act 1986 (c. 41), s. 109(5) and Sch. 21

- F98Word repealed by Finance Act 1983 (c. 28), ss. 35(3)(c), 48(5), Schs. 7 para. 1 and Sch. 10 Part III

- M411980 c. 1.

- F99Words substituted by Finance Act 1983 (c. 28), s. 35 and Sch. 7 para. 2

- M421980 c. 1.

- F100Words in Sch. 19 para. 3(1) inserted (27.7.1999 with effect as mentioned in s. 99(2) of the amending Act) by 1999 c. 16, s. 99(1)(a)

- F101Words in Sch. 19 para. 3(1) inserted (27.7.1999 with effect as mentioned in s. 99(2) of the amending Act) by 1999 c. 16, s. 99(1)(a)

- F102Sch. 19 para. 3(1A) inserted (27.7.1999 with effect as mentioned in s. 99(2) of the amending Act) by 1999 c. 16, s. 99(1)(b)

- M431983 c.56.

- M441968 c. 13.

- M451970 c. 9.

- C24See Advance Petroleum Revenue Tax Act 1986 (c. 68, SIF 63:1), s. 1(6)

- F103Words substituted by Finance Act 1989 (c. 26), s. 180(2)(d)(7)—deemed always to have had effect

- M461980 c. 48.

- M471981 c. 35.

- M481980 c. 1.

- M491980 c. 1.

- C25See also Advance Petroleum Revenue Tax Act 1986 (c. 68, SIF 63:1) for the repayment of certain amounts of APRT

- F104Words substituted by Finance Act 1983 (c. 28), s. 35 and Sch. 7 para. 3

- M501980 c. 1.

- M511980 c. 48.

- M521980 c. 48.

- C26Part of the text of Sch. 19 Part II para. 16(2)–(4) is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- F105Words substituted by Finance Act 1983 (c. 28), s. 35 and Sch. 7 para. 4

- C27Part of the text of Sch. 19 Part III paras. 18 and 21 is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- C28Part of the text of Sch. 19 Part III paras. 18 and 21 is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- M531980 c. 1.

- M541971 c. 29.

- F106Sch. 20 para. 4(2) repealed by Finance Act 1989 (c. 26), s. 187(1) and Sch. 17 Pt. XIII

- C29The text of Sch. 20 is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and, except as specified, does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- F107Sch. 21 repealed by Capital Allowances Act 1990 (c. 1, SIF 63:1), s. 164(4) and Sch. 2

- C30The text of Sch. 22 Pts. I, IV, VIII and XI is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- C31Part of the text of Sch. 22 Pts. II, III, VII and X is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- C32Part of the text of Sch. 22 Pts. II, III, VII and X is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- C33The text of Sch. 22 Pts. I, IV, VIII and XI is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- C34Part of the text of Sch. 22 Pts. II, III, VII and X is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- C35The text of Sch. 22 Pts. I, IV, VIII and XI is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- C36Part of the text of Sch. 22 Pts. II, III, VII and X is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- C37The text of Sch. 22 Pts. I, IV, VIII and XI is in the form in which it was originally enacted: it was not reproduced in Statutes in Force and does not reflect any amendments or repeals which may have been made prior to 1.2.1991

- M551972 c. 20.

- M561972 c. 20.

- F108S. 152(3) repealed (10.7.2003) by Finance Act 2003 (c. 14), Sch. 43 Pt. 5(5)

- F109S. 156 repealed (22.7.2004) by Statute Law (Repeals) Act 2004 (c. 14), Sch. 1 Pt. 5 Group 18

- F110Words in s. 11(1) substituted (15.1.2007) by Fraud Act 2006 (c. 35), s. 15(1), Sch. 1 para. 19; S.I. 2006/3200, art. 2

- F111Sch. 1 repealed (21.7.2008) by Statute Law (Repeals) Act 2008 (c. 12), Sch. 1 Pt. 8

- F112S. 1(3) repealed (21.7.2008) by Statute Law (Repeals) Act 2008 (c. 12), Sch. 1 Pt. 8

- F113S. 3 repealed (21.7.2008) by Statute Law (Repeals) Act 2008 (c. 12), Sch. 1 Pt. 8

- F114S. 137 repealed (21.7.2008) by Statute Law (Repeals) Act 2008 (c. 12), Sch. 1 Pt. 8

- F115S. 150 repealed (21.7.2008) by Statute Law (Repeals) Act 2008 (c. 12), Sch. 1 Pt. 8

- F116Words in s. 129(1) omitted (with effect in accordance with s. 99(2) of the amending Act) by virtue of Finance Act 2008 (c. 9), Sch. 32 para. 12 (with Sch. 32 para. 22(1)(c))

- F117S. 4(2) omitted (1.11.2008) by virtue of Finance Act 2008 (c. 9), Sch. 6 paras. 8(a), 21

- F118S. 4(3) omitted (1.11.2008) by virtue of Finance Act 2008 (c. 9), Sch. 6 paras. 8(a), 21

- F119S. 4(7) omitted (1.11.2008) by virtue of Finance Act 2008 (c. 9), Sch. 6 paras. 8(a), 21

- F120Words in Sch. 18 para. 10(1) substituted (1.4.2009) by The Finance Act 2008, Schedule 40 (Appointed Day, Transitional Provisions and Consequential Amendments) Order 2009 (S.I. 2009/571), art. 1(1), Sch. 1 para. 8(1)

- F121Sch. 18 para. 10(2)(b) omitted (1.4.2009) by virtue of The Finance Act 2008, Schedule 40 (Appointed Day, Transitional Provisions and Consequential Amendments) Order 2009 (S.I. 2009/571), art. 1(1), Sch. 1 para. 8(2)

- F122Words in Sch. 18 para. 8(1) omitted (1.4.2009) by virtue of The Transfer of Tribunal Functions and Revenue and Customs Appeals Order 2009 (S.I. 2009/56), art. 1(2), Sch. 1 para. 101(2)

- F123Word in Sch. 18 para. 8(3) substituted (1.4.2009) by The Transfer of Tribunal Functions and Revenue and Customs Appeals Order 2009 (S.I. 2009/56), art. 1(2), Sch. 1 para. 101(3)

- F124Words in Sch. 18 para. 8(4) substituted (1.4.2009) by The Transfer of Tribunal Functions and Revenue and Customs Appeals Order 2009 (S.I. 2009/56), art. 1(2), Sch. 1 para. 101(4)(a)(i)

- F125Word in Sch. 18 para. 8(4) substituted (1.4.2009) by The Transfer of Tribunal Functions and Revenue and Customs Appeals Order 2009 (S.I. 2009/56), art. 1(2), Sch. 1 para. 101(4)(a)(ii)

- F126Words in Sch. 18 para. 8(4)(a) substituted (1.4.2009) by The Transfer of Tribunal Functions and Revenue and Customs Appeals Order 2009 (S.I. 2009/56), art. 1(2), Sch. 1 para. 101(4)(b)(i)

- F127Words in Sch. 18 para. 8(4)(a) substituted (1.4.2009) by The Transfer of Tribunal Functions and Revenue and Customs Appeals Order 2009 (S.I. 2009/56), art. 1(2), Sch. 1 para. 101(4)(b)(ii)

- F128Words in Sch. 18 para. 8(4)(b) substituted (1.4.2009) by The Transfer of Tribunal Functions and Revenue and Customs Appeals Order 2009 (S.I. 2009/56), art. 1(2), Sch. 1 para. 101(4)(c)

- F129Word in Sch. 18 para. 8(4)(c) substituted (1.4.2009) by The Transfer of Tribunal Functions and Revenue and Customs Appeals Order 2009 (S.I. 2009/56), art. 1(2), Sch. 1 para. 101(4)(d)

- F130Words in Sch. 18 para. 8(5) inserted (1.4.2009) by The Transfer of Tribunal Functions and Revenue and Customs Appeals Order 2009 (S.I. 2009/56), art. 1(2), Sch. 1 para. 101(5)(a)

- F131Words in Sch. 18 para. 8(5) inserted (1.4.2009) by The Transfer of Tribunal Functions and Revenue and Customs Appeals Order 2009 (S.I. 2009/56), art. 1(2), Sch. 1 para. 101(5)(b)

- F132Words in Sch. 19 para. 7(1) omitted (1.4.2009) by virtue of The Transfer of Tribunal Functions and Revenue and Customs Appeals Order 2009 (S.I. 2009/56), art. 1(2), Sch. 1 para. 102(2)

- F133Words in Sch. 19 para. 7(2) inserted (1.4.2009) by The Transfer of Tribunal Functions and Revenue and Customs Appeals Order 2009 (S.I. 2009/56), art. 1(2), Sch. 1 para. 102(3)(a)

- F134Sch. 19 para. 7(2)(e) and word inserted (1.4.2009) by The Transfer of Tribunal Functions and Revenue and Customs Appeals Order 2009 (S.I. 2009/56), art. 1(2), Sch. 1 para. 102(3)(f)

- F135Words in Sch. 19 para. 7(2)(a) substituted (1.4.2009) by The Transfer of Tribunal Functions and Revenue and Customs Appeals Order 2009 (S.I. 2009/56), art. 1(2), Sch. 1 para. 102(3)(b)

- F136Words in Sch. 19 para. 7(2)(b) substituted (1.4.2009) by The Transfer of Tribunal Functions and Revenue and Customs Appeals Order 2009 (S.I. 2009/56), art. 1(2), Sch. 1 para. 102(3)(c)

- F137Word in Sch. 19 para. 7(2)(c) omitted (1.4.2009) by virtue of The Transfer of Tribunal Functions and Revenue and Customs Appeals Order 2009 (S.I. 2009/56), art. 1(2), Sch. 1 para. 102(3)(d)

- F138Words in Sch. 19 para. 7(2)(c) substituted (1.4.2009) by The Transfer of Tribunal Functions and Revenue and Customs Appeals Order 2009 (S.I. 2009/56), art. 1(2), Sch. 1 para. 102(3)(e)

- F139Words in Sch. 19 para. 7(2)(d) substituted (1.4.2009) by The Transfer of Tribunal Functions and Revenue and Customs Appeals Order 2009 (S.I. 2009/56), art. 1(2), Sch. 1 para. 102(3)(e)

- F140Words in s. 134(1) substituted (with effect in accordance with s. 381(1) of the amending Act) by Taxation (International and Other Provisions) Act 2010 (c. 8), s. 381(1), Sch. 8 para. 178 (with Sch. 9 paras. 1-9, 22)

- F141Words in s. 134(1) inserted (with effect in accordance with s. 1184(1) of the amending Act) by Corporation Tax Act 2010 (c. 4), s. 1184(1), Sch. 1 para. 177 (with Sch. 2)

- F142Sch. 19 para. 10(7) repealed (with effect in accordance with s. 381(1) of the amending Act) by Taxation (International and Other Provisions) Act 2010 (c. 8), s. 381(1), Sch. 8 para. 179, Sch. 10 Pt. 6 (with Sch. 9 paras. 1-9, 22); and also repealed (with effect in accordance with s. 1184(1) of the amending Act) by Corporation Tax Act 2010 (c. 4), s. 1184(1), Sch. 1 para. 178, Sch. 3 Pt. 2 (with Sch. 1 para. 178(2), Sch. 2)

- F143Words in s. 129(1) substituted (with effect in accordance with art. 3 of the commencing S.I.) by Finance Act 2010 (c. 13), Sch. 6 paras. 8, 34(2); S.I. 2012/736, art. 3

- F144Words in s. 129(1) omitted (1.4.2012) by virtue of The Public Bodies (Abolition of the National Endowment for Science, Technology and the Arts) Order 2012 (S.I. 2012/964), arts. 1(2), 3(1), Sch.

- F145Sch. 19 para. 2(4A) inserted (with effect in accordance with s. 140(4) of the amending Act) by Finance Act 2016 (c. 24), s. 140(3)

- F146Word in s. 140 substituted (1.10.2016) by The Petroleum (Transfer of Functions) Regulations 2016 (S.I. 2016/898), regs. 1(2), 6(2)

- F147Word in Sch. 19 para. 3(1)(a) substituted (1.10.2016) by The Petroleum (Transfer of Functions) Regulations 2016 (S.I. 2016/898), regs. 1(2), 6(3)

- F148Sch. 6 Pt. 4 omitted (1.4.2026) by virtue of Finance Act 2026 (c. 11), s. 88(3), Sch. 13 para. 2(b) (with Sch. 13 para. 21)

- F149S. 8(1)(c) omitted (1.4.2026) by virtue of Finance Act 2026 (c. 11), s. 88(3), Sch. 13 para. 2(a) (with Sch. 13 para. 21)